Working capital is a business’s investment in “current assets”, less the capital provided by carrying “current liabilities”. Current assets typically include cash held in operating accounts, inventory and accounts receivable. Current liabilities is the amount payable to trade, plus other short term financial accommodations, such as bank loans.

The amount of working capital fluctuates due to many things. A change in sales volume can cause a change in receivables, and potentially inventory. And a change in production volume, or a change in vendor payment terms, can also cause working capital requirements to fluctuate.

“Permanent” working capital is the normal or “standard” amount of investment in current assets less current liabilities. It assumes a steady, unchanging level of sales and production activity and no changes in terms of trade. With an understanding and quantification of permanent working capital, one can then monitor or project fluctuations around the norm to better manage a business’s cash flow and funding requirements.

If a fluctuation around the norm is a short term phenomenon, it will reverse itself over the short term. And when the reversal occurs, the cash flow and funding effect of the initial change will be reversed. If a fluctuation is permanent, then the cash flow and funding effect will be permanent, it will not reverse itself.

Understanding whether a change in working capital is temporary or permanent is critical to management of cash flow and a business’s funding strategy. Investment in permanent working capital is no different than investment in any other long term asset, like machinery and equipment, and funding for that investment should be long term. But temporary fluctuations in working capital can be safely met with short term debt, or even a temporary change in cash on hand.

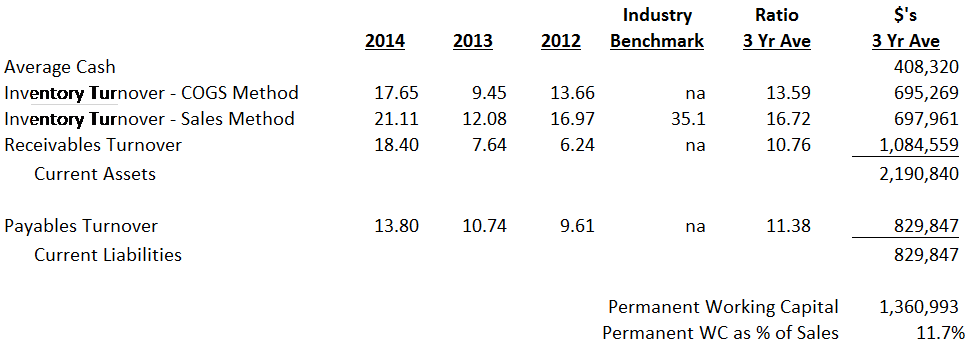

The following lays out a sample calculation of permanent working capital. Note that averaging three YE numbers, as is done in this example, is not a good practice. Business activity may have changed significantly in more recent times, and when using only 3 measurements, any one could inappropriately skew the calculation. Twelve month end measures over the last year, or perhaps 18 over the last year and a half, is likely to provide a more reliable calculation.

Also note that, in this hypothetical case, permanent investment in inventory is high compared to industry averages. If this business could reduce its normal inventory, it could achieve a reduction in permanent working capital required, freeing up capital for other purposes.

JCJCo provides business and financial strategy consulting services to emerging entrepreneurial and middle market companies, in many cases in the role of “Outsourced CFO”. If your business has evolved to the point where greater financial management expertise is required, JCJCo can fill that need at a cost that is “right sized” for your business.

Joseph C. Jessup

8/30/15

Leave a Reply